How did investors view the reforms and supervisory organisations of the late nineteenth century?

Home > How did investors view the reforms and supervisory organisations of the late nineteenth century?

by Avni Önder Hanedar (Sakarya University)

In the last couple of decades, high debt burden in emerging economies created financial crises and the low growth rate during the 2008 financial crisis led to a default problem for Greece. Some reforms were proposed, such as institutional changes and the establishment of an entity under control of the other Eurozone members to supervise the repayment of debts. These events have some similarities with the default of the Ottoman Empire and the establishment of the Ottoman Public Debt Administration (OPDA) (Düyun-u Umumiye). To deal with the inefficiencies in the Ottoman economy and political system, reforms were implemented, as supervisory organizations were established during the nineteenth century. Important ones were the adoption of the gold standard in 1880, the Administration of Six Indirect Revenues (Rüsum-u Sitte) (ASIR) in 1879, and the OPDA in 1881. It seems that many of them were not seen by investors as promising, since a British weekly magazine, Punch or The London Charivari, illustrated these events as bubbles. A paper of Elmas Yaldız Hanedar, Avni Önder Hanedar, and Ferdi Çelikay examined how such events were perceived at the İstanbul bourse, which could shed light on today’s realities.

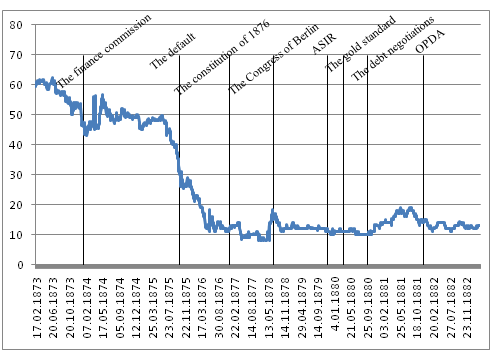

The paper manually collected historical data on the price of the General Debt bond traded at the İstanbul bourse between 1873 and 1883 from volumes of daily Ottoman newspapers, i.e., Basiret, Ceride-i Havadis, and Vakit. This bond was the most actively traded one at the İstanbul bourse in 1881, during the foundation of the OPDA.

The paper is the first to measure in econometrically sophisticated manner investors’ beliefs at the İstanbul bourse in reference to the reforms and financial control organizations. Historical research does not include detailed empirical information for the effects of reforms and financial control organizations on the İstanbul bourse during the default period. Using unique data on the most actively traded Ottoman government bond, the paper extends the historical literature on the İstanbul bourse (See Hanedar et al. (2017)) and reforms (See Mauro et al. (2006), Birdal (2010), Mitchener and Weidenmier (2010) looking at bond markets in multiple developing countries, with samples that include the Ottoman Empire).

The methodology in the paper was to analyse the variance of returns (derived from the price showed in above) as a proxy of financial instabilities and risks. To model volatility, the paper estimated a GARCH model with dummy variables for reforms and financial control organizations at and after the dates of the events (i.e., short- and long-run).

The empirical results indicated a permanent decrease in volatility after the establishment of the OPDA and the gold standard. The foundation of a locally controlled finance commission in 1874 was correlated with a lower volatility level at the date of the event, but increased volatility in the long term. The Ottoman case is instructive for the understanding of today’s economic situation in emerging markets such as Greece, while it could be argued that long-lived and comprehensive measures with foreign creditors’ supervision on fiscal and monetary systems matter more for investors’ perceptions. Lowering government interventions on economic system and transaction costs due to bimetallism were viewed as promising. Investor beliefs that the local and short-lived reforms and supervisory organizations were ineffective could be due to several factors such as lack of measures to limit public expenditures.

References

Vakit. (6 October 1875). Sarafiye, Galata piyasası, 2.

Birdal, M. (2010). The Political economy of Ottoman public debt, insolvency and European control in the late nineteenth century. London: I. B. Tauris and Co Ltd.

Hanedar, A. Ö., Hanedar, E. Y., Torun, E., & Ertuğrul, H. M. (2017). Dissolution of an Empire: Insights from the İstanbul Bourse and the Ottoman War Bond. Defence and Peace Economics, (Forthcoming).

Mauro, P., Sussman, N., & Yafeh, Y. (2006). Emerging markets and financial globalization: Sovereign bond spreads in 1870-1913 and today. Oxford: Oxford University press.

Mitchener, K. J. & Weidenmier, M. D. (2010). Super sanctions and sovereign debt repayment. Journal of International Money and Finance, 29(1), 19–36.