Taxation, fiscal capacity and credible commitment in eighteenth-century China: the effects of the formalization and centralization of informal surtaxes

Home > Taxation, fiscal capacity and credible commitment in eighteenth-century China: the effects of the formalization and centralization of informal surtaxes

by Max Hao (Peking University) and Kevin Liu (The Hong Kong University of Science and Technology).

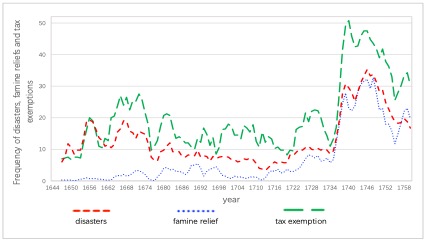

In premodern Europe, famine relief was inadequately provided until the late 19th century. In contrast, in late imperial China, preventing starvation helped legitimate the state and played a key role in reducing internal conflicts. The Qing state operated a network of granaries and developed sophisticated procedures to report famines and supply relief. However, as shown in Figure 1, the frequency of famine relief recorded in the Qingshilu (veritable records of Qing) was much lower than the frequency of disasters under the reigns of Shunzhi (1644-1661) and Kangxi (1661-1722). In contrast, in the reign of Yongzheng (1723-1735) and in the early years of Qianlong (1736-1760), famine relief became more responsive to disasters. Why did the Qing state take on the responsibility for “nourishing the people” only after 1723?

To solve this puzzle, we explore the effect of a reform that formalized and centralized part of the fiscal system in premodern China: the ‘huohao turned to public’ reform instituted in Emperor Yongzheng’s reign (1723-1735). ‘Huohao’ denotes all the informal surtaxes collected by county governments. Because the bulk of formal tax revenue was remitted directly to the central government, provincial and county governments retained only a limited share of this income with limited discretion over its expenditure. Consequently, they imposed huohao or surtaxes to finance their own expenses. However, because these informal revenues were unsanctioned and unmonitored by the central government, they were largely pocketed by officials.

The ‘huohao turned to public’ reform was an endeavor to formalize huohao in order to achieve two interconnected policy goals: to reduce corruption and enhance provincial fiscal capacity by centralizing control. First, huohao was collected at rates designated by the provincial governor and delivered to the provincial treasury. Second, 60% of the remitted funds were allocated to county magistrates and provincial governors as ‘anticorruption salaries’ to finance their regular expenses, reducing their incentive to collect informal surtaxes and seize public revenues. More importantly, 40% of the formalized houhao was assigned as public funds to finance irregular expenses at the governors’ discretion. The total annual revenue from the formalized huohao amounted to 4.5 million taels of silver, of which 1.8 million were reserved as public funds. In sum, by formalizing and centralizing informal surtaxes, the reform enhanced provincial fiscal capacity by giving provincial governors more resources and a greater incentive to spend them on public goods. The design of the reform is illustrated in Figure 2.

Because corruption is extremely difficult to explore empirically, we mainly focus on whether the second goal was achieved. The timing of when the reform was initiated and completed differed between provinces, but the reasons behind these variations were largely exogenous to provincial characteristics, enabling us to use them to test the effects of reform. We test whether the huohao reform raised the frequency of famine relief in periods of disastrous weather by exploiting the different timing of the reform process across provinces. We restrict our dataset to 1710-1760, when the bulk of famine relief was financed by the provinces.

Using a prefecture-level panel dataset, we find that in times of extreme drought and floods, the frequency of famine relief increased after the reform by 1.05 times per prefecture, which was more than 100% of the standard deviation of the dependent variable relative to that under non-disastrous weather. By exploring the dynamics of the reform’s impact, we find no pre-trend, which supports the exogeneity of the reform’s timing. Our results are robust to controlling for other initiatives by the central government, such as tax exemptions, the allocation of tribute grain and central fiscal revenues, the enforcement of bureaucratic monitoring, and other concurrent fiscal reforms. We also find that famine relief effectively reduced grain prices when disasters occurred, indicating that public funds were spent on famine relief which had a beneficial impact on the population. Further, we find that the reform’s impact was greater when areas faced exceptional flooding compared to exceptional droughts, and greater in prefectures which had difficulties collecting taxes, suggesting that the reform facilitated the intertemporal and spatial redistribution of financial resources.

For this tax reform to have a sustained effect on provincial government capacity, central government would need to resist the expropriation of these new revenues for its own use. However, in premodern China, there were no institutional constraints on this dispossession. After emperor Qianlong (1736-1796) succeeded to the throne, the central government began to make regular checks on the expenditure of provincial public funds, forced the inter-provincial transfers of funds, and expended them on projects previously financed by central revenues. These actions forced provincial governments to reduce their expenditure on famine relief and withhold anticorruption salaries meant for county administrators. This finding highlights that it was the lack of credible commitment that accounted for the short-lived success of this fiscal reform. Viewed from this perspective, the reform provides a valuable lesson about the role of political institutions in the Great Divergence.

To contact the authors:

Max Hao (maxhao1003@pku.edu.cn)

Kevin Liu (kevin.liu@connect.ust.hk)