UK investment trust portfolio strategies before the first world war

Home > UK investment trust portfolio strategies before the first world war

by Janette Rutterford and Dimitris P. Sotiropoulos (The Open University Business School)

The full article from this blog has been published in the Economic History Review.

—

UK investment trusts (the British name for closed-end funds) were at the forefront of financial innovation in the global era before World War I. Soon after the increase in investment choice facilitated by Companies Acts in the 1850s and 1860s – which allowed investors limited liability – investment trusts emerged to invest in a diverse range of securities across the globe, thereby offering asset management services to individual investors. They rapidly became a low-cost financial vehicle for so-called “averaging” of risk across a portfolio of marketable securities without having to sacrifice return. UK investment trusts were the first genuine historical paradigm of a sophisticated asset management industry.

Formed as trusts from the the late 1860s, by the 1880s, the vast majority of UK investment trusts had acquired limited liability company status and issued shares and bonds traded in London and elsewhere. They used the proceeds to construct global investment portfolios made up of a multitude of different securities whose yields were higher than could be achieved by investing solely in British securities, an approach subsequently termed the ‘geographical diversification of risk’.

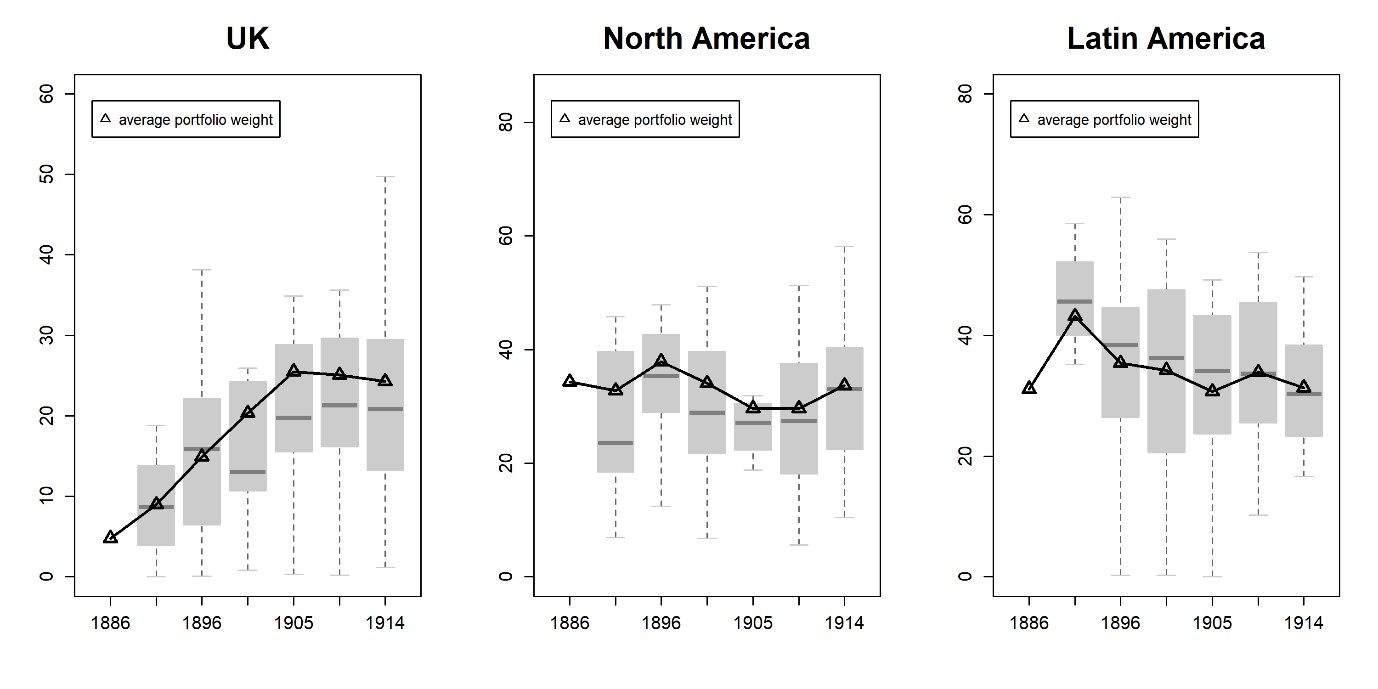

A recent study of ours examines UK investment trust portfolio strategies between 1886 and 1914, for those investment trusts that disclosed their portfolios. Our dataset comprises 30 different investment trust companies, 115 firm portfolio observations, and 32,708 portfolio holdings, sampled every five years prior to WWI. Our results reveal a sophisticated approach to asset management by these investment trusts. The average trust in our sample had a portfolio with a nominal value of £1.7 million – equivalent to around £1.7bn today – invested in an average of 284 different securities. Their size and the large number of holdings are both evidence that asset management before WWI was a serious business.

Investment trusts evolved a unique asset allocation strategy: globally diversified, skewed in favour of preferred regions, sectors and security types, and with numerous holdings. Figure 1 shows the flow of investment from Europe to the emerging North and Latin American markets over the period, although the box plots reveal significant differences between individual investment trust portfolios. The preference for overseas investments is clear: on average, domestic investment never exceeded 26 percent of portfolio value. Railways was the preferred sector, averaging 40 percent of portfolio value throughout the period. Government and municipal securities fell out of favour from a high of 40 percent in 1886 to a low of sic percent of portfolio value by 1914. Investment trusts switched instead to the Utilities and the Industrial, Commercial and Agriculture sectors which, combined, made up 48 percent of portfolio value by 1914.

Figure 2 shows the types of securities held in investment trust portfolios. Fixed-interest securities dominated before WWI, though there was a growing interest in ordinary and preferred shares over time. Perhaps surprisingly, an increasing number of investment trusts were willing to embrace the ‘cult of equity’, far earlier than, say, insurance companies.

We find that investment trust directors adopted a mixture of a buy-and-hold investment and active portfolio management strategies. The scale of holdings of a wide variety of different types of securities required efficient administration. The average portfolio holding represented only 0.35 percent of portfolio value, while 75 percent of holdings had individual weights of less than 0.43 percent of portfolio value. Although not concentrated, these portfolios were skewed. The top 10 percent of holdings per portfolio represented on average 35.7 percent of total portfolio value, and the top 25 percent of holdings represented 60.0 percent.

Investment trust directors did not radically reorganize their portfolios on an annual basis; neither did they stick rigidly to the same securities over time. They were not passive investors. Annual turnover was in excess of 10 percent (measured as the lower of sales and purchases to nominal portfolio value). Nor were they sheep. There was a wide variety of focus between different UK investment trusts; each tended to have its own specific investment areas of interest, and there was considerable cross-sectional variation with respect to diversification strategies, even though joint directorships were common.

Was this approach good for the investor? We compared the returns and risk-adjusted returns of three unweighted samples of companies: investment trusts, banks and ‘other’ financial firms and found that investing in investment trust shares surpassed the other alternatives, whether risk-adjusted or not. Our results offer evidence that the specific goal of investment trusts – the global distribution of risk – was certainly beneficial to their investors in the period up to WWI.

This early foray into fund management by UK investment trusts was deemed a success, but UK investment trusts only represented around one percent of total London Stock Exchange capitalization by 1914. It is an interesting open question as to why it took decades for the asset management industry to take-off. A focus on different episodes in the history of investment trusts can help shed more light on the – under-researched – evolution of the asset management industry. This will allow economic historians, fund managers, and policy-makers to draw lessons from how history affects the evolutionary path of modern financial practices.

—

To contact the authors:

Janette Rutterford, j.rutterford@open.ac.uk

@jrutterford

Dimitris P. Sotiropoulos, dimitris.sotiropoulos@open.ac.uk

@dpsotiropoulos