The German bank-growth nexus revisited: Savings banks and economic growth in Prussia

Home > The German bank-growth nexus revisited: Savings banks and economic growth in Prussia

by Sibylle Lehmann-Hasemeyer and Fabian Wahl (University of Hohenheim)

The full article from this blog has been published in The Economic History Review and is now available through Open Access.

—

The German banking system is often considered a key factor in German industrialisation. For Alexander Gerschenkron, Germany’s experience can serve as a role model for other moderately backward economies: governments could trigger economic development by supporting the establishment of modern financial institutions such as universal banks, which were typical of the German banking system and which mobilised savings, reduced risks for investors, and improved the allocation of resources. Such activities ease the trading of goods and services and foster technological innovation.

Scholarly discussion on the banking-growth nexus in Germany has focused on universal banks without giving significant attention to other forms of banking. It is surprising that earlier research has ascribed savings banks a limited role in industrialization: by 1913, they held 24.8 per cent of the total assets of all German financial institutions and ranked first among all bank types for net investment. Moreover, savings banks had the advantage of being public institutions. Because they were not profit-driven, they could focus on long-term projects with high social returns.

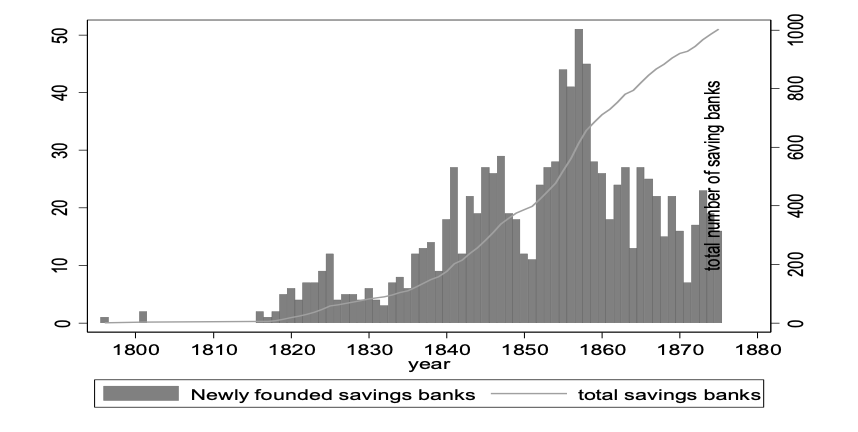

Our study revisits the banking-growth nexus by focusing on savings banks in 978 Prussian cities. We found a positive and significant relationship between the establishment of savings banks and city growth, and the number of steam engines per factory in the nineteenth century (1854-75). Previous research has either studied the impact of savings banks at a highly aggregated level or qualitatively with case studies. This study is the first to provide quantitative evidence on the local impact of savings banks during the early nineteenth century.

To address potential endogeneity, we refer to a decree issued in 1854 by the Minister for Trade and Commerce. This decree enhanced the equal distribution of saving, because it demanded the founding of at least one savings bank per county. It further encouraged poorer local authorities to found a savings bank by offering institutional and financial support. Following this decree, a wave of savings banks were established on a much wider geographical distribution than before. In 1849, savings banks were present in about half of the counties; this had risen to nearly 95 per cent by 1864.

We also observed a significant pre-growth trend in earlier periods before the founding of a savings bank in a city. There is no such trend, however, after 1854 (Figure 1).The savings banks that were founded during this wave were often established in smaller cities that might not have been able to afford them without support. Thus, the decree can be seen as a public policy to promote the establishment of public financial infrastructure in remote regions.

Although we cannot perfectly solve the endogeneity issue, the regression results suggest that savings banks promoted city growth. This is even more plausible when considering that Germany’s industrialisation was not only based on larger, multinational firms and coal resources, but rather on good public infrastructure, a competitive schooling system, and, in particular, on small and medium-sized firms, which were the backbone of German industry. The resulting economic landscape persists today.

Our study contributes to the understanding of why Germany industrialised by analysing a neglected aspect of the relationship between banks and growth. Earlier research, which focussed on the impact of large universal banks and stock markets at the end of the 19th century, largely overlooking the impact of savings banks and the potential benefit of a decentralised financial system. The evidence that we provide clearly shows that there is a considerable gap in the literature on savings banks and how they actually contributed to economic growth.

—

To contact the authors:

Sibylle Lehmann-Hasemeyer, sibylle.lehmann@uni-hohenheim.de

Fabian Wahl, fabian.wahl@uni-hohenheim.de

{kind=link}